The US dollar jumped sharply on Wednesday after the Federal Reserve, in its first meeting under Chair Kevin Warsh, held interest rates steady but signaled that a rate hike could be on the table later this year. The shift in tone triggered a broad repricing across FX markets as traders reduced expectations for any near-term easing.

Market snapshot

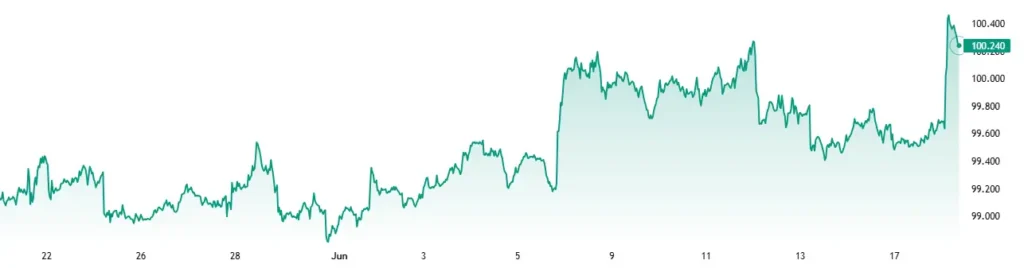

The US Dollar Index (DXY) climbed toward the 99.50–100 region as yields rose and rate-hike expectations increased. Risk assets sold off, with US equities broadly lower, while the dollar strengthened against major peers including the euro, yen, and sterling. Treasury yields moved higher as markets adjusted to a more hawkish Fed outlook.

“Markets were positioned for a neutral-to-dovish hold, but the Fed effectively removed the easing bias and introduced a credible hike scenario,” said one FX strategist, noting the shift was more important than the unchanged rate decision itself.

Event details: Warsh’s first policy shift

The Federal Reserve kept the benchmark rate unchanged at 3.50%–3.75%, marking a fourth consecutive hold. However, policymakers revised forward expectations, with a growing number of officials signaling at least one rate increase before the end of 2026.

The new Fed statement also dropped its previous easing bias and shortened forward guidance, reflecting Chair Warsh’s preference for a less explicit communication framework. Market participants said the absence of a clear dovish path forced a rapid reassessment of rate expectations.

“The message is simple: inflation is still too sticky, and the Fed is no longer leaning toward cuts,” another trader said.

FX reaction: dollar dominance returns

The dollar strengthened broadly as the prospect of higher-for-longer US rates regained traction. EUR/USD slipped, while USD/JPY extended gains amid widening rate differentials. Sterling also weakened against the greenback.

Analysts said the dollar’s move was amplified by positioning unwind, as investors had been pricing in potential cuts later in the year. The shift back toward a possible hike scenario forced rapid dollar covering.

Equities and risk assets under pressure

US equities declined in response to tighter policy expectations. The S&P 500 (SPX) fell more than 1% intraday, led by rate-sensitive technology and growth sectors. Banks initially outperformed on higher yield expectations but also gave back gains as broader risk sentiment deteriorated.

Bond markets also reflected the shift, with short-end yields rising more sharply than long-end, flattening yield curves as traders priced in reduced policy easing.

Macro implications: inflation still in focus

The Fed’s tone reinforced concerns that inflation remains persistently above target, with energy-linked price pressures and resilient demand complicating the disinflation path. The updated projections suggest policymakers are less confident that inflation will return quickly to 2%.

Economists noted that the policy shift reduces the likelihood of rate cuts in 2026 and increases the probability of a more extended restrictive cycle if inflation remains elevated.

Outlook risks: policy uncertainty rises

Markets now face heightened uncertainty around the Fed’s reaction function under Warsh, particularly after the removal of traditional forward guidance tools. This leaves incoming data—especially inflation and labor reports—more influential in driving expectations.

Traders will now focus on:

- Upcoming US CPI and PCE inflation readings

- Federal Reserve speaker commentary following the meeting

- Further movement in Treasury yields and DXY around the 100 level

For now, the dollar remains supported, but analysts warn that volatility may stay elevated as markets adjust to a less predictable Fed framework.