(By ATFX Analyst Team)

Key TakeawaysCeasefire Violations: On Tuesday, the Iranian Foreign Ministry told US strikes on Iran’s southern Hormozgan province were a “gross violation” of the fragile ceasefire that had held for nearly seven weeks, while the US countered that the action was defensive. The news largely dampened hopes for an imminent deal to end the nearly three-month conflict. Consumer Sentiment Drops: US consumer confidence fell in May amid inflation fears sparked by the war with Iran. Households generally hold a more pessimistic view of the labor market, though conditions are expected to improve before the end of the year. Today’s Focus: The Reserve Bank of New Zealand (RBNZ) decided to leave interest rates unchanged but noted that the official cash rate may need to be hiked sooner and by a larger margin than previously projected. For intraday data, market participants can look to the US Richmond Fed Manufacturing Index for May, while the market simultaneously braces for tomorrow’s release of the US PCE price index and revised GDP figures. |

Global Market Review 27/05/2026

The S&P 500 and the Nasdaq closed at historic highs on Tuesday, buoyed by Artificial Intelligence (AI) amid lingering market anxieties about the peace talks. US Treasury yields edged lower, while the US Dollar Index (DXY) rose 0.13% to 99.16.

Spot gold fell more than 1%. Prices were weighed down by uncertainty over the US-Iran peace deal and mounting expectations of a Fed interest rate hike. WTI crude finished lower, whereas Brent crude pushed higher. Markets were initially spooked by concerns that US airstrikes on Iran would derail peace negotiations, though trading remained mixed by the close.

Key Events Today:

- 08:00 BoJ Gov Ueda Speech ***

- 09:30 AU CPI APR ***

- 10:00 RBNZ Interest Rate Decision ***

- 22:00 US Richmond Fed Manufacturing Index MAY **

May 28th

- 04:30 API Crude Oil Stock Change ***

- 15:20 ECB President Lagarde Speech ***

- 17:00 EU Economic Sentiment MAY **

- 20:10 US Building Permits APR **

- 20:30 US GDP & PCE Price Index 2nd Est Q1 ***

- 20:30 US Core PCE Price Index APR ***

- 20:30 US Initial Jobless Claims ***

- 22:00 US New Home Sales APR **

Markets Analysis 27/05/2026

- Resistance: 1.1655/1.1676

- Support: 1.1600/1.1584

Yesterday, the EUR/USD retreated from a four-day high as renewed tensions in the Middle East appeared to offset the impact of hawkish ECB rate expectations. In the early Asian session on Wednesday, the pair rebounded slightly and consolidated around 1.1640.

Analyst View: The pair continues to trade near the 10-day moving average, a pivotal level where short-term bulls and bear’s clash. An upside breakout could pave the way for a move towards resistance above 1.1655, whereas a break below would threaten the 1.1600 handle and support levels.

Bias: Consolidation mode

- Resistance: 1.3522/1.3564

- Support: 1.3386/1.3343

Yesterday, the GBP/USD retreated from a near two-week high, recording its steepest decline in over a week amid renewed tensions in Iran. However, the pair attempted a rebound this morning and is trading around 1.3440 in early trading.

Analyst View: With the 10-day moving average acting as support for two consecutive days, being held above this level could trigger a short-term rebound. However, the 20-day moving average has also recently acted as resistance. For now, attention remains on the pair’s consolidation within the range between these two moving averages.

Bias: Range-bound

- Resistance: 159.39/159.73

- Support:159.06/158.62

Speaking this morning, the BOJ Governor said that the impact of a rise in oil prices can vary depending on factors such as wages, inflation expectations, demand, and exchange rates. The USD/JPY rebounded yesterday, tracking broader US dollar strength, and closed at its highest level since late April.

Analyst View: After hitting fresh highs yesterday, the pair is poised to extend gains above 159.50. However, if an upside breakout approaches the critical 160 psychological handle, intervention fears are expected to cap further gains.

Bias: Mildly bullish

- Resistance: 94.98/96.93

- Support: 91.11/88.66

Crude oil prices closed lower overnight, partly under technical pressure, despite market anxieties that the US-Iran peace agreement process could be derailed following US airstrikes in southern Iran.

Analyst View: Crude hit its lowest intraday level since May 6 yesterday. Although it bounced from its low of $89.40, it ultimately failed to close higher. As long as prices remain capped below $95, oil will face near-term downside pressure. Market participants should stay focused on headline risk, which could trigger volatility.

Bias: Consolidation at lows

- Resistance: 4572/4605

- Support: 4468/4435

- Resistance: 78.75/80.79

- Support: 74.72/72.17

Gold prices fell over 1% yesterday and continued to edge toward $4,500 this morning, pressured by the Fed’s rate hike expectations and a fresh US military strike against Iran that dampened hopes for a peace agreement.

Analyst View: Gold sild from a one-week high yesterday and failed to break above the top of its main range over the past two weeks, indicating that bears remain in control. With the 10-day moving average still acting as resistance, near-term gold prices are poised to move lower. Attention should be paid to last week’s low range, which may offer support again.

Bias: Short–term bearish

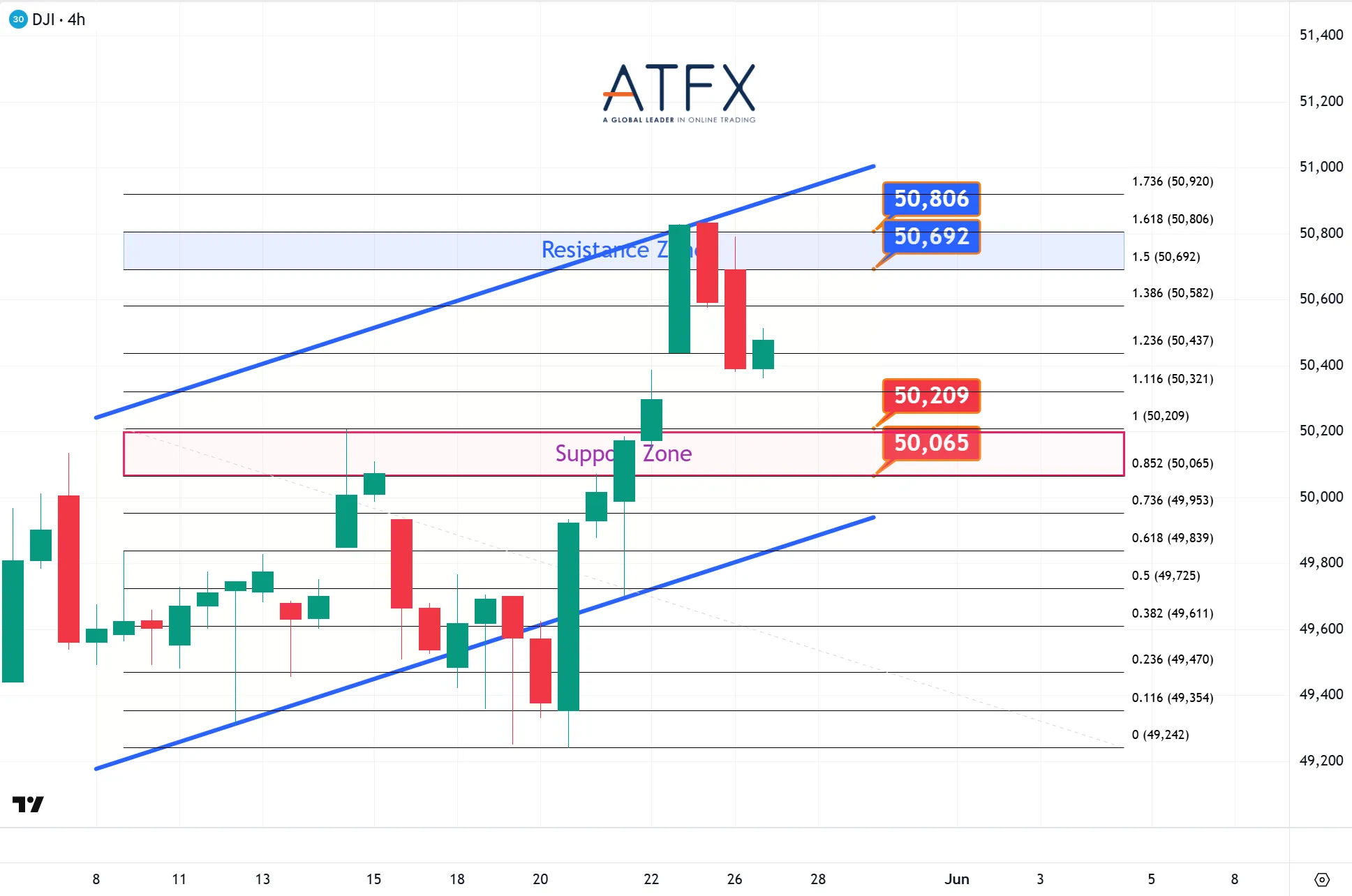

- Resistance: 50692/50806

- Support: 50209/50065

Yesterday, market sentiment was initially lifted by expectations of a US-Iran peace agreement and strong momentum in the AI sector. However, Dow failed to sustain these gains overnight, retreating by over 100 points amid expectations of a Fed rate hike and setbacks in the US-Iran peace process.

Analyst View: Dow snapped a four-day winning streak yesterday, recording its largest single-day drop in more than a week. After giving up the 51,000 handle, the key question is whether this short-term correction will gain traction. On the downside, the 10-day moving average near 50,100 serves as a critical defensive line.

Bias: Short-term correction

- Resistance: 30286/30786

- Support: 29499/29006

Tech stocks rallied sharply overnight, fueled by a retreat in US Treasury yields and a major price-target upgrade from UBS. Market sentiment was further boosted when Micron Technology briefly crossed the $1 trillion market-cap threshold for the first time on Tuesday. Despite uncertainty clouding hopes for a US-Iran peace process, the Nasdaq still reached a fresh record high.

Analyst View: Nasdaq opened higher and gained momentum throughout yesterday’s session, reaching a new record high and officially breaking above the 30,000 psychological milestone. The current upside target shifts to the 30,286/30,786 resistance range. However, market participants should note that uncertainty surrounding the peace agreement, alongside a wait-and-see approach ahead of tomorrow’s US PCE price index release, could cap further significant gains.

Bias: Bullish at highs

- Resistance: 77944/78881

- Support: 73991/73039

Bitcoin fell below $77,000 on Tuesday as renewed U.S. strikes on Iranian targets dented hopes for a near-term peace deal, while cooling inflows into exchange-traded funds added to pressure on the world’s largest cryptocurrency.

Analyst View: BTC/USD gave back its gains after hitting a five-day high yesterday, recording its steepest four-day drop. Technically, the pair remains capped by the top of its recent one-week range. Following a trend-matching break below the 10-day moving average, short-term downside momentum could follow, shifting focus to support levels below 74,000.

Bias: Short-term correction

Enjoy trading! The content is for reference only. Please ensure that you understand the risk.