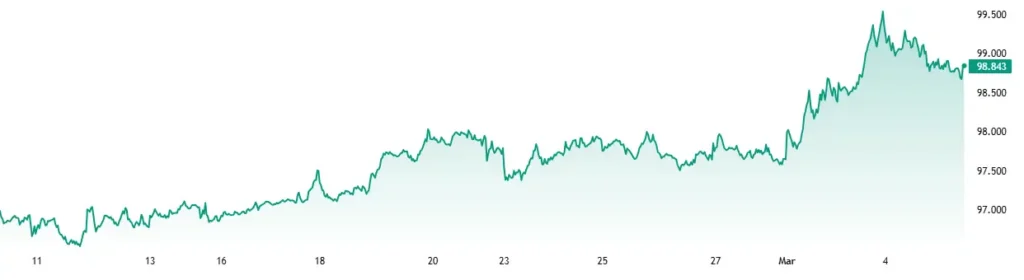

The U.S. dollar eased on Wednesday, with the Dollar Index (DXY) slipping toward 98.80 even after stronger-than-expected U.S. private payrolls and services data, as investors focused instead on the inflation and growth risks from the widening U.S.-Iran war and disruptions around the Strait of Hormuz . Safe-haven demand stayed firm for bullion, while oil remained near multi-month highs and Treasury yields held elevated as traders reassessed the path for Federal Reserve cuts.

Market snapshot

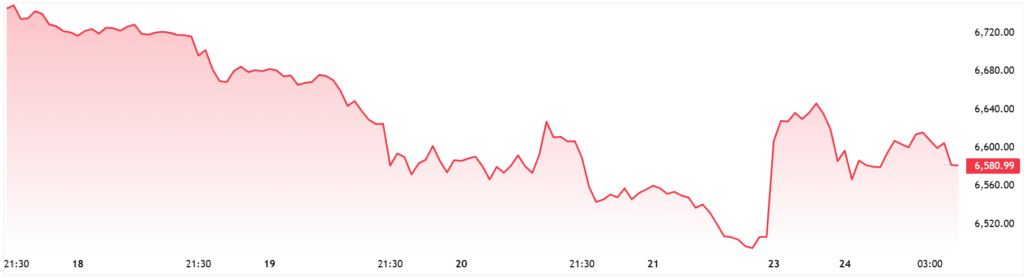

The dollar’s retreat followed a two-day rebound that had briefly pushed DXY close to 100.00, but by late U.S. trade it was back near 98.80 . EUR/USD recovered to around 1.1640, GBP/USD steadied near 1.3370, and USD/JPY slipped to roughly 156.78-157.00 as the greenback gave back some haven gains . Gold added to its rebound, rising 0.8% to $5,176.69 an ounce, while Brent crude (LCOc1) settled flat at $81.40 a barrel after earlier touching $84.48; U.S. crude (CLc1) ended up 0.1% at $74.66 .

Equities painted a more nuanced picture. U.S. stocks rebounded, with the S&P 500 (SPX) up 0.78% at 6,869.50, the Nasdaq Composite (IXIC) up 1.29% at 22,807.48 and the Dow Jones Industrial Average (DJI) up 0.49% at 48,739.41, helped by hopes that diplomacy could cap the oil shock. In Europe, the STOXX 600 (.STOXX) rose 1.4%, recovering part of the prior session’s war-driven selloff.

Data strength, but markets look through it

The immediate trigger for the initial dollar support was a run of firm U.S. data. ADP said private payrolls increased by 63,000 in February, above expectations, while the ISM services PMI climbed to 56.1 from 53.8, its highest since July 2022 and well above the 53.5 consensus. The figures reinforced the view that the U.S. economy entered the first quarter with solid momentum.

But markets treated the data as secondary to geopolitics. “The U.S. economy is off to a decent start,” BMO’s Sal Guatieri said, while warning that the Iran war remained a downside risk if energy prices spike further. That helps explain why the dollar failed to extend gains despite the stronger macro backdrop.

Oil, yields and inflation worries

The bigger macro story remains the oil shock. Shipping through the Strait of Hormuz has been effectively paralysed for five days, and Iraq has already cut output by nearly 1.5 million barrels per day because exports have stalled. Reuters also reported Brent hit its highest settlement since January 2025, underscoring how quickly the conflict has fed into energy pricing and inflation expectations.

That has rippled across bonds. The benchmark U.S. 10-year Treasury yield rose to 4.098%, while the 2-year yield climbed to 3.551%, as traders cut near-term easing bets and worried that higher oil could slow disinflation . Bill Northey of U.S. Bank Wealth Management said markets were watching whether rates move higher on “an unanchoring of inflation expectations” tied to hydrocarbons.

Policy path and broader implications

The data and the oil backdrop now argue in opposite directions for central banks: growth has held up, but energy-driven inflation risks have intensified. Reuters reported the Fed is still expected to hold rates steady at its March 17-18 meeting, while rate-cut timing has been pushed back, with some investors now looking for the first move in July or later and others seeing no fully priced cut until September.

For broader assets, the message is similar. Risk appetite can revive when oil pauses and diplomacy headlines emerge, but defensive demand remains close beneath the surface, supporting gold and the yen while keeping volatility sensitive to any new escalation. Jim Awad of Clearstead Advisors said White House efforts to steady oil markets had offered relief, but added the optimism “will be tested over the coming weeks”.

Key monitors

Traders will now watch Thursday’s U.S. jobless claims and Friday’s February nonfarm payrolls report, where economists in a Reuters poll expect payrolls growth of 59,000 and unemployment steady at 4.3%. They will also track any sign of restored Hormuz shipping flows or further supply disruption, and whether oil’s resilience feeds more directly into inflation pricing, Fed expectations and renewed pressure on global equities and bonds.