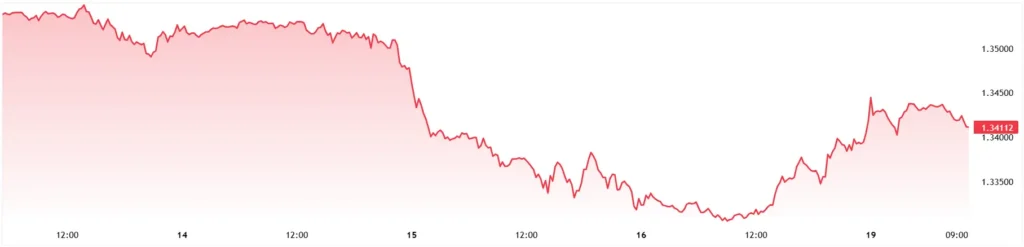

Sterling recovered on Monday as investors weighed a sharp rise in UK government bond yields against mounting political pressure on Prime Minister Keir Starmer and uncertainty over the Bank of England’s next move.

The GBP/USD pound rebounded from around $1.3300 in Asian trading to about $1.3450 by the New York close, reversing much of last week’s decline. The move came despite renewed selling in gilts, with higher yields reflecting concerns over Britain’s fiscal outlook and a possible Labour leadership contest.

UK assets have been unsettled since Labour’s poor local election results earlier in May. Wes Streeting resigned as health secretary on May 14 and said he was prepared to stand if a leadership contest is triggered. Greater Manchester Mayor Andy Burnham is also positioning for a possible return to Parliament, while former deputy prime minister Angela Rayner has re-emerged as a potential contender after resolving a tax issue.

Bond investors are focused on whether a change in Labour leadership could bring looser fiscal policy, higher borrowing or a shift toward greater state spending. Those concerns have pushed gilt yields to multi-year highs, raising the cost of financing Britain’s debt and narrowing the government’s room for manoeuvre.

For currency markets, however, higher yields have also reinforced expectations that the Bank of England may have less scope to cut interest rates. The BoE held Bank Rate at 3.75% on April 30, with its next decision due on June 18.

Comments from BoE officials on Monday underlined divisions on the Monetary Policy Committee. Megan Greene warned central banks should not assume inflationary shocks from the Iran war will prove temporary, while Sarah Breeden has emphasised weaker growth risks. Catherine Mann, one of the committee’s more hawkish voices, has continued to stress inflation persistence.

The next test for sterling will come from UK labour market data on Tuesday and inflation figures on Wednesday. Markets expect regular pay growth to cool to 3.4% from 3.6%, the unemployment rate to hold at 4.9%, and headline CPI to ease to 3.0% from 3.3%.

A stronger inflation or wages reading could bolster expectations of a June rate increase and support sterling. Softer data would likely challenge the rebound and revive pressure on the pound, particularly if political uncertainty keeps gilts under strain.

The broader risk is that the currency and bond markets begin sending different signals, with sterling supported by rate expectations, while gilt prices reflect fiscal stress. That split could narrow quickly if investors conclude higher yields reflect political risk rather than stronger monetary policy support.