Market Highlight 23/01/2026

U.S. consumer spending grew steadily in both November and October, as households increased purchases across a wide range of goods and services. This suggests the economy may maintain strong growth for a third consecutive quarter. Major U.S. stock indices closed higher on Thursday, rising for a second straight day. Investor buying was boosted after U.S. President Trump withdrew tariff threats against European allies, while data highlighted the resilience of the U.S. economy. The Dow Jones rose 0.6%, the S&P 500 gained 0.55%, and the Nasdaq Composite advanced 0.9%. The U.S. dollar weakened, while the euro and British pound strengthened.

Gold prices broke above $4,900 per ounce for the first time, supported by geopolitical tensions, a weaker dollar, and expectations of Federal Reserve rate cuts. Silver also hit a record high. Spot gold settled at $4,921.51 per ounce, up 1.76%. Oil prices pulled back after Trump softened his threats toward Greenland and Iran,and as signs emerged that the Russia–Ukraine war could be nearing a resolution.

Key Outlook 23/01/2026

Today’s focus is on the Bank of Japan’s interest rate decision. After raising rates by 25 basis points in December last year, expectations for further hikes have cooled as markets factor in political considerations. While some believe the BoJ could hike again in the near term to address yen weakness, the market widely expects rates to remain unchanged at this meeting. The decision statement is expected to mention the yen exchange rate, and particular attention will be on comments from Governor Kazuo Ueda.

Key Data and Events Today:

- 11:00 BoJ Interest Rate Decision ***

- 14:30 BOJ Press Conference ***

- 15:00 GB Retail Sales MoM DEC **

- 16:30 EU GERMANY Manufacturing & Services PMI PREL JAN **

- 17:00 EU Manufacturing & Services PMI PREL JAN **

- 17:30 GB Manufacturing & Services PMI PREL JAN **

- 22:45 US Manufacturing & Services PMI PREL JAN ***

- 23:00 US Michigan Consumer Sentiment Final JAN *** steady

Key Data and Events Coming Week:

- Monday: Australia Holiday, Germany Ifo Business Climate JAN, US Durable Goods Orders DEC, US Dallas Fed Manufacturing Index JAN

- Tuesday: US CB Consumer Confidence JAN, US New Home Sales DEC, US Richmond Fed Manufacturing Index JAN

- Wednesday: API Crude Oil Stock Change, BoJ Monetary Policy Meeting Minutes, AU CPI DEC, Germany GfK Consumer Confidence FEB, BoC Interest Rate Decision, BoC Press Conference, EIA Crude Oil Stocks Change

- Thursday: Fed Interest Rate Decision, Fed Press Conference, Germany GfK Consumer Confidence FEB, EU Economic Sentiment JAN, US Initial Jobless Claims, US Balance of Trade NOV, US Factory Orders NOV

- Friday: JP Unemployment Rate DEC, Germany Unemployment Rate DEC, Germany GDP QoQ Flash Q4, EU GDP Preliminary Q4, Germany CPI Preliminary JAN, US PPI DEC, CA GDP NOV

Markets Analysis 23/01/2026

- Resistance: 1.1808/1.1834

- Support: 1.1692/1.1664

EUR/USD fell 0.49% to 1.1744 as Trump softened his stance on Greenland, easing geopolitical fears, while steady US PCE and consumption limited deeper USD losses. Price rebounded from the 1.1664–1.1692 support zone and may retest descending resistance near 1.1808–1.1834.

- Resistance: 1.3535/1.3568

- Support: 1.3456/1.3429

GBP/USD rose 0.24% to 1.1357 as US–EU trade de-escalation lifted risk appetite after Trump signaled a Greenland deal with NATO; strong US GDP/jobs still didn’t support the Dollar amid Fed easing bets. Price bounced from 1.3429 and is climbing back into the range, but supply remains heavy near 1.3535–1.3568. Above that zone keeps upside traction alive; rejection risks a slip back toward 1.3450.

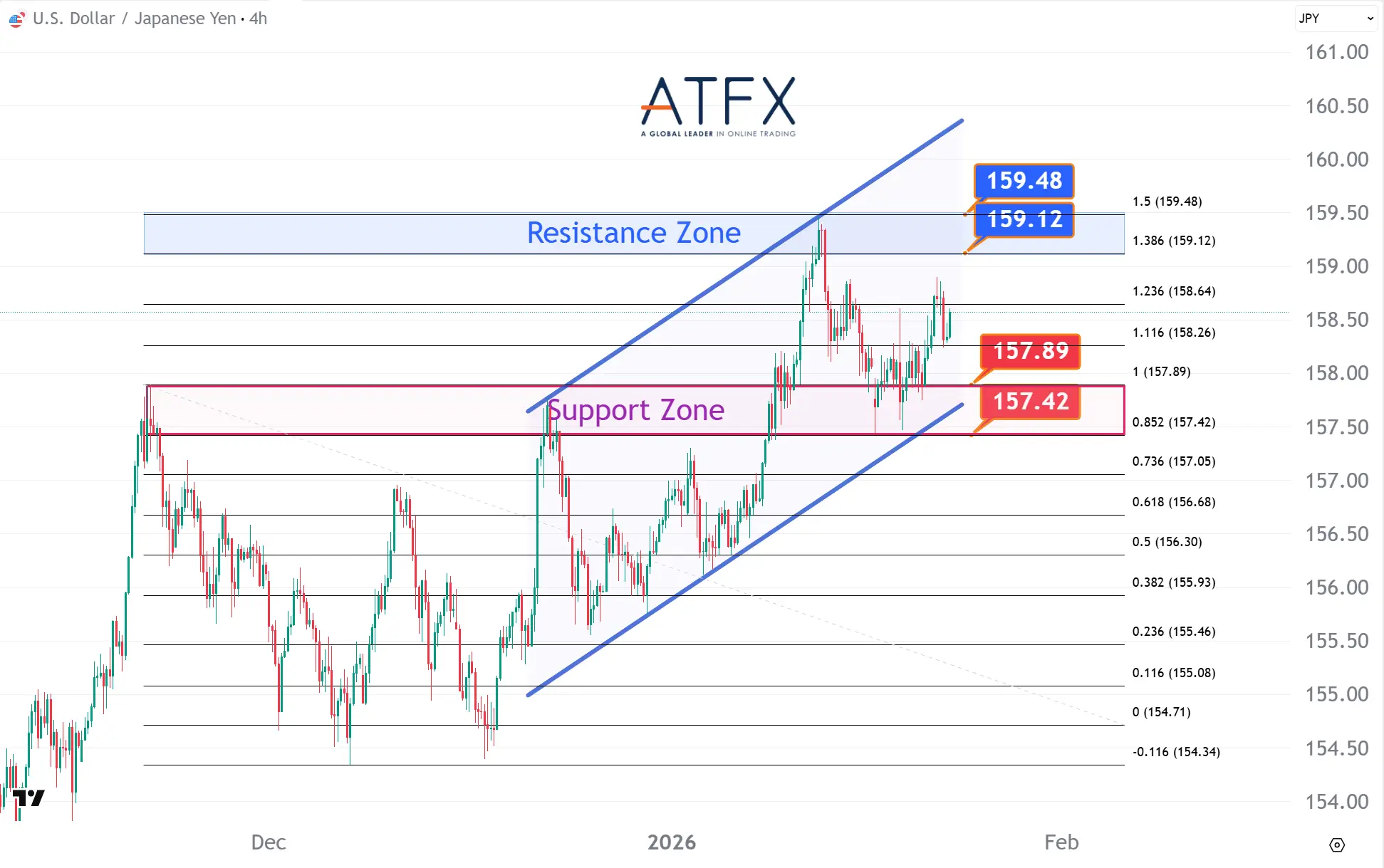

- Resistance: 159.12/159.48

- Support: 157.89/157.42

USD/JPY slipped to 158.42 and remains near recent lows as markets watch for a potential hawkish shift from the BoJ, while rising super-long bond prices add pressure. Price is holding above the 157.42 area but keeps running into selling interest near 159.12–159.48. A break higher would revive upside momentum, while failure risks another dip toward 157.42.

- Resistance: 60.60/61.48

- Support: 58.65/57.78

WTI fell 2.1% to $59.36, hitting a one-week low as Trump softened rhetoric on Greenland and Iran, reducing geopolitical risk premiums. Hopes of progress toward ending the Russia–Ukraine war raised supply concerns and added pressure. Price is sliding within a descending channel, with rebounds capped near 60.60–61.48, while a break below 57.78 could open deeper downside.

- Resistance: 5077/5132

- Support: 4833/4775

- Resistance: 102.71/105.40

- Support: 93.61/90.88

Gold surged to a record high of $4,959.81 and is trading near $4,942, supported by rising geopolitical tensions, a weaker dollar, and Fed rate-cut expectations. Price is pushing higher within an ascending channel after holding above the 4,775–4,833 support zone. A sustained break could open a run toward the 5,077–5,132 resistance area.

- Resistance: 49789/50109

- Support: 49075/48750

The Dow Futures rose 0.63% for a second straight session as Trump withdrew tariff threats, lifting risk appetite, while upward GDP revision and resilient consumption supported equities. Price is holding within an ascending channel after bouncing from the

48,750–49,075 support zone. A push above 49,789–50,109 could extend gains, while failure risks a pullback toward 48,750.

- Resistance: 25736/25879

- Support: 25261/25116

The NAS100 climbed 0.91% as large tech stocks rallied, and optimism over US economic resilience lifted growth shares. Investors now focus on upcoming tech earnings for fresh direction. Price has bounced from the 25261–25116 support zone but remains capped near 25,736–25,879 resistance.

- Resistance: 92787/94759

- Support: 86439/84440

Bitcoin slipped 0.6% to $89,295, falling below $90,000 again as the Greenland de-escalation rally faded and momentum stalled. Despite improved risk sentiment, BTC lagged the global equity rally and struggled to regain traction above the $92,787–$94,759 resistance zone. Price is stabilizing above the 86,439–84,440 support area, but a failure to reclaim $90,000 risks renewed downside pressure.

Enjoy trading! The content is for reference only. Please ensure that you understand the risk.