Market Highlight 16/01/2026

U.S. initial jobless claims unexpectedly fell last week. Although the labour market remains largely stagnant, the data further reinforced expectations that the Federal Reserve will keep interest rates unchanged in the coming months. U.S. equities advanced on Thursday, led by strong quarterly earnings from Morgan Stanley and Goldman Sachs, which pushed their shares sharply higher. Solid results from Taiwan Semiconductor Manufacturing Company (TSMC) also boosted U.S. chip stocks. The Dow Jones Industrial Average rose 0.6%, the S&P 500 gained 0.26%, and the Nasdaq Composite increased 0.25%. The U.S. dollar climbed to a six-week high, rising 0.24% to 99.31, while EUR/USD fell 0.31% to 1.1606.

Gold prices edged lower as the drop in U.S. initial jobless claims supported the dollar, while U.S. President Donald Trump’s more conciliatory tone on Iran further dampened safe-haven demand. Spot gold slipped 0.1% to USD 4,614.62 per ounce. International oil prices retreated sharply, ending a five-day winning streak. Trump said Iran’s crackdown on protesters appeared to be easing, reducing market concerns over potential military action and disruptions to oil supply.

Key Outlook 16/01/2026

During the European session, Germany will release its final December CPI figures, with the annual rate expected to hold at 2% and the monthly rate at zero. A moderation in inflation would reduce the urgency for the European Central Bank to shift its policy stance. Later in the day, attention will turn to U.S. December industrial production, expected to post a modest 0.2% month-on-month increase, offering insight into whether manufacturing activity is emerging from stagnation.

Key Data and Events Today:

- 15:00 EU GERMANY CPI MoM Final DEC **

- 22:15 US Industrial Production MoM DEC **

Key Data and Events Coming Week:

- Monday: US Holiday, CN Retail Sales & Industrial Production DEC, CN GDP YoY Q4, JP Industrial Production MoM NOV, EU CPI Final DEC, CA CPI DEC

- Tuesday: CN Loan Prime Rate (1Y & 5Y) JAN, GB Unemployment Rate NOV, Germany PPI DEC, EU ZEW Economic Sentiment Index JAN

- Wednesday: NYMEX Crude Oil February Futures Expiry, US API Crude Oil Stock Change, GB CPI & PPI DEC, IEA Monthly Oil Market Report, US Pending Home Sales DEC, US Building Permits SEP

- Thursday: EIA Crude Oil Stocks Change, AU Unemployment Rate DEC, ECB Meeting Minutes, US GDP & Core PCE Prices Final Q3, US Initial Jobless Claims

- Friday: JP CPI DEC, JP Manufacturing & Services PMI Flash JAN, BoJ Interest Rate Decision, BoJ Press Conference, GB Retail Sales DEC, Germany Manufacturing & Services PMI Prelim JAN, EU Manufacturing & Services PMI Prelim JAN, GB Manufacturing & Services PMI Prelim JAN, US Manufacturing & Services PMI Prelim JAN, US Michigan Consumer Sentiment Final JAN, EU Consumer Confidence Flash JAN

Markets Analysis 16/01/2026

EURUSD

- Resistance: 1.1643/1.1666

- Support: 1.1570/1.1541

EUR/USD slipped towards 1.1613 as a surprise drop in U.S. jobless claims lifted the dollar to a six-week high. Technically, the pair remains within a clear descending channel, with rebounds capped by the 1.1643–1.1666 resistance zone. If this zone holds, downside pressure persists, with focus on the 1.1570–1.1541 support area.

GBPUSD

- Resistance: 1.3440/1.3470

- Support: 1.3312/1.3282

GBP/USD remains under pressure as broad USD strength continues to dominate. Price action shows fading rebounds below recent swing highs, with selling interest returning quickly. Unless the pair regains ground above 1.3440, downside risks remain skewed toward the 1.3312–1.3282 area.

USDJPY

- Resistance: 159.26/159.66

- Support: 157.89/157.37

USD/JPY remains elevated as USD strength and expectations of fiscal expansion in Japan continue to weigh on the yen. Technically, momentum faded after the push towards 159, with choppy price action signalling hesitation at higher levels. Holding above the 157.37–157.89 area keeps the bias firm, though intervention risk makes upside progress uneven.

US Crude Oil Futures (FEB)

- Resistance: 60.78/61.57

- Support: 58.27/57.49

WTI crude plunged more than 3% as easing rhetoric on Iran and sharply higher U.S. crude and gasoline inventories erased geopolitical risk premiums. Technically, the rally above $61 was swiftly rejected, with prices sliding back below $59, signalling a clear loss of upside momentum. Unless WTI reclaims the $60.78–61.57 area, downside risks remain dominant, with support at $58.27–57.49.

Spot Gold

- Resistance: 4656/4687

- Support: 4550/4509

Spot Silver

- Resistance: 94.09/95.69

- Support: 87.18/85.52

Gold pulled back from record highs as strong U.S. labour data and easing geopolitical tensions reduced safe-haven demand. Technically, price stalled near the $4,650 area and entered consolidation. Holding above the $4,550–4,509 zone keeps the broader bullish structure intact.

Dow Futures

- Resistance: 50088/50404

- Support: 48742/48431

The Dow Futures rose on strong bank earnings, with results from Goldman Sachs, Morgan Stanley and BlackRock boosting risk sentiment. Technically, the index remains in an uptrend but faces resistance near the 50,088–50,404 zone. Failure to clear this zone may keep price action range-bound in the near term.

NAS100

- Resistance: 25835/25973

- Support: 25380/25240

The NAS100 edged higher, supported by gains in chipmakers, though sector rotation continues to cap upside. Technically, price stalled near the 25,835–25,973 resistance

zone, indicating persistent selling pressure. Failure to reclaim this zone leaves the index in consolidation, with support at 25,380–25,240.

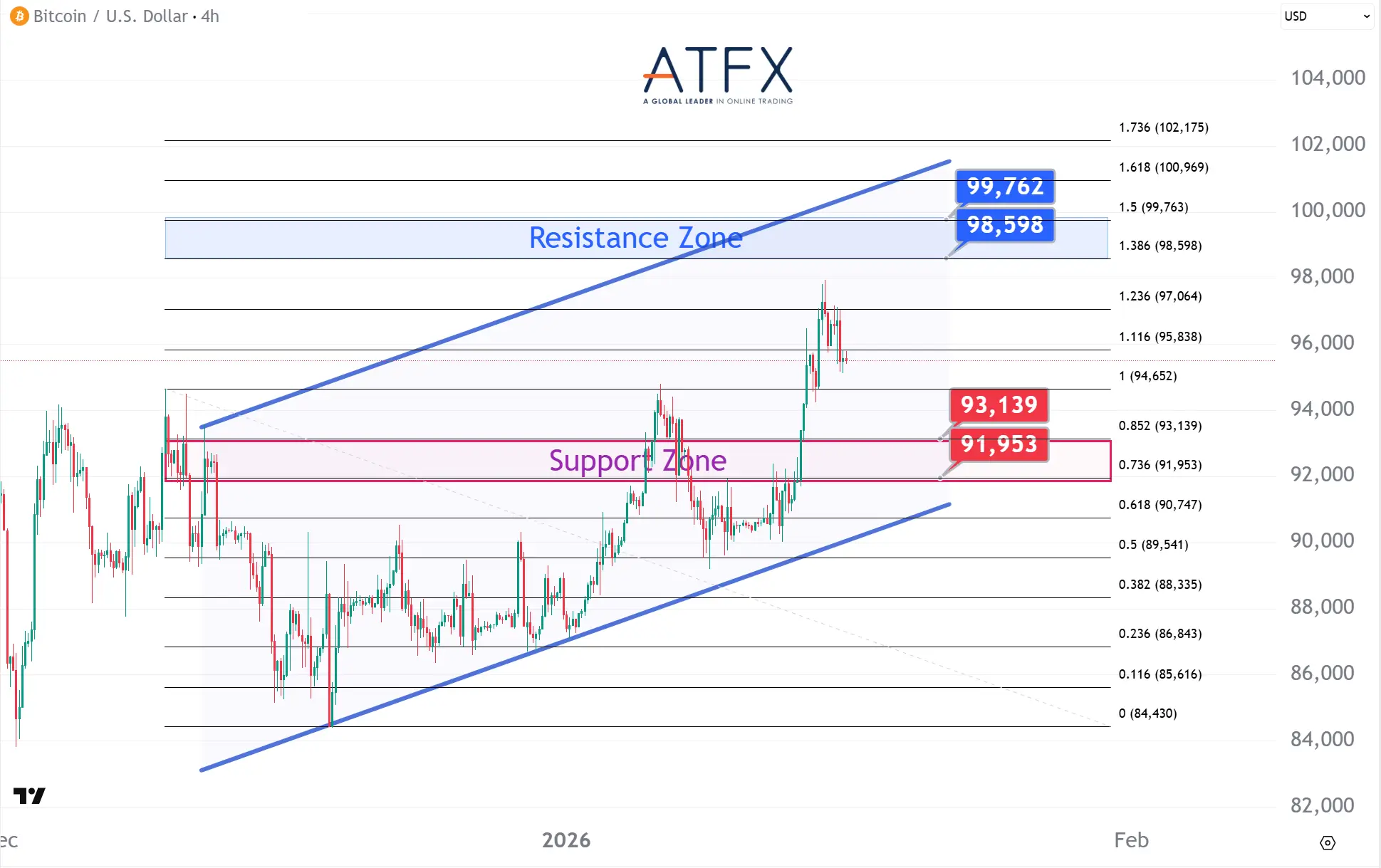

BTC

- Resistance: 98598/99762

- Support: 93139/91953

Bitcoin steadied around $95,500 as markets assessed developments on a proposed U.S. crypto bill, with policy uncertainty keeping risk appetite fragile. Recent gains were underpinned by Strategy’s large purchase, though upside momentum remains cautious. Technically, price holds above the $93,139–91,953 support zone, while resistance at 98,598–99,762 continues to cap rallies.

Enjoy trading! The content is for reference only. Please ensure that you understand the risk.